Savers could flock to ‘risk-free’ NS&I ahead of £20,000 ISA rule change

Analysts are claiming savers could flock to Premium Bonds once a £20,000 ISA rule change comes into effect next despite a recent rate cut from National Savings and Investments (NS&I).

Earlier this week, the Government-backed financial institution confirmed the prize fund rate attached to the savings product will be reduced in April 2026 from 3.6 per cent to 3.3 per cent.

As a result of this decision, the chances of someone winning for each £1 Bond will also deteriorate, moving from 22,000 to one to 23,000 to one in a major blow to customers.

While the monthly draw continues to dangle the possibility of substantial prizes, including £50,000, £100,000, or the sought-after £1million jackpots, the reality remains that numerous savers go extended periods without receiving any winnings at all.

Do you have Premium Bonds?

|

NS&I / GETTY

While these reduced prospects may encourage some to consider alternative savings options, analysts note looming changes to ISA rules could lead to Premium Bonds becoming more attractive.

Michele Tieghi, financial expert and founder of psyfi money, shared: “Premium Bonds offer a safe investment, as you can’t lose money. It’s also great for those who might need quick access to their cash, as you can take your money out of Premium Bonds at any time.

“However, the downside to Premium Bonds is that there is no guaranteed income.”

According to Mr Tieghi, someone placing £20,000 into Premium Bonds could expect average annual prize winnings somewhere between £600 and £900.

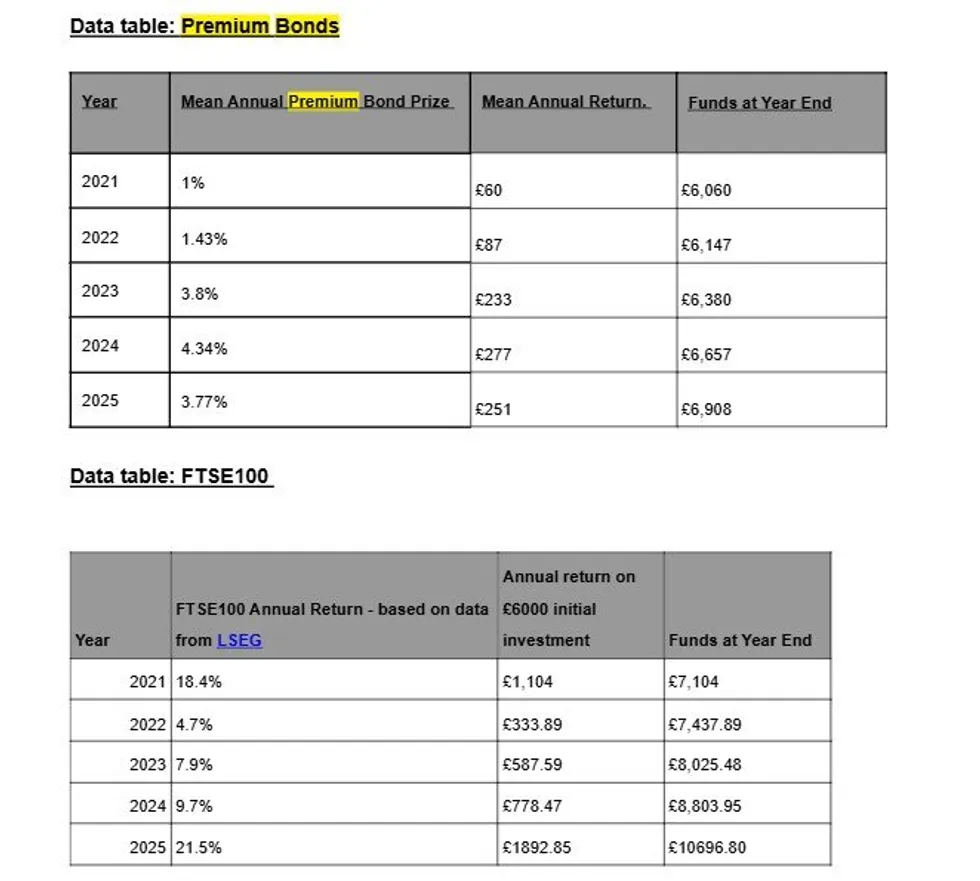

How have Premium Bonds compared to the Ftse 100? | LIGHTYEAR

How have Premium Bonds compared to the Ftse 100? | LIGHTYEAR  Premium Bonds holders can check to see if they have won a prize via the Premium Bonds prize checker app | NSI

Premium Bonds holders can check to see if they have won a prize via the Premium Bonds prize checker app | NSIDuring the Autumn Budget 2025, Chancellor Rachel Reeves announced that from April 2027, the ISA allowance structure will be significantly altered. Currently, savers can place up to £20,000 annually across cash ISAs and stocks and shares ISAs in whatever proportion they prefer.

Under the new system, only £12,000 can be deposited flexibly, with the remaining £8,000 required to go into investment-based accounts.

However, individuals aged 65 and over will be exempt from these restrictions and will continue to benefit from the existing allowance arrangements.

The ISA changes could drive more savers towards Premium Bonds as a risk-free option, according to Mr Tieghi.

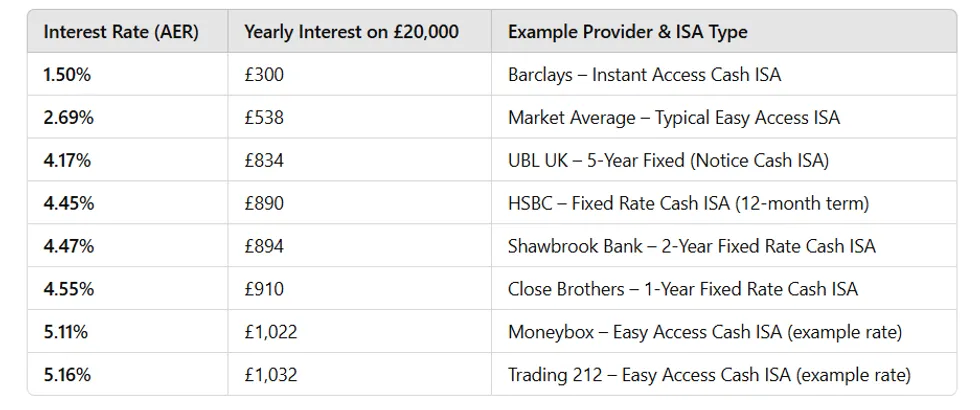

Examples of tax free Isa earnings in the UK if you had £20,000 in the Isa | GBN

Examples of tax free Isa earnings in the UK if you had £20,000 in the Isa | GBNHe explained: “The new cash ISA limit in 2027 could cause more people to put their money into Premium Bonds. If they previously invested £20,000, and they’re quite a safe investor, then they will be keen to look at risk-free alternatives.”

Mr Tieghi suggested savers might split their money, placing £12,000 in a cash ISA and £8,000 into Premium Bonds.

Currently, easy-access cash ISAs are offering rates reaching 4.4 per cent, which would yield £880 annually on a £20,000 deposit, though rates are anticipated to decline further.

Mr Tieghi cautioned that additional prize rate cuts this year could see returns drop to between 2.5 and 3 per cent.