ISA hack could boost YOUR savings pot by £33,700: ‘Huge difference!’

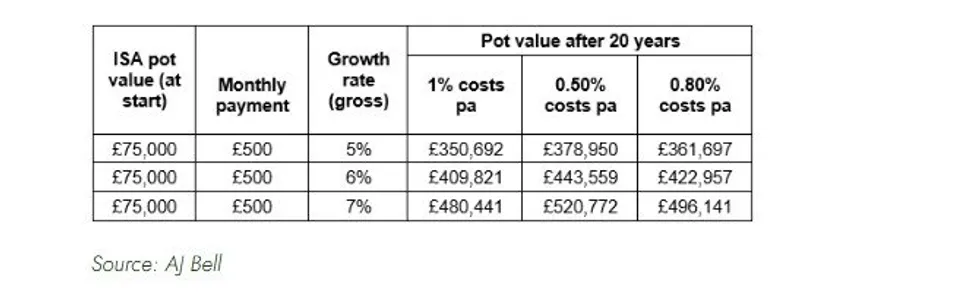

Investors holding stocks and shares ISAs could find themselves more than £33,700 better off over two decades simply by trimming their annual charges by half a percentage point.

This calculation assumes a portfolio valued at £75,000 with monthly contributions of £500, according to analysis from AJ Bell.

The scale of potential savings is significant given that close to £1trillion sits in UK ISA products, with 15 million adults adding fresh funds during the 2023/24 tax year.

Charlene Young, senior pensions and savings expert at AJ Bell, said: “Shopping around for the best value stocks and shares ISA for your needs just like you might in other areas of your daily life can make a huge difference to the future value of your tax-free investment pot.”

AJ Bell is sharing ISA hacks which could make a ‘huge difference’ for your savers

|

GETTY

Ms Young outlined five practical strategies for reducing costs, starting with a shift towards passive investments. Tracker funds and ETFs typically carry charges of around 0.1 per cent annually, compared with approximately 0.75 per cent for actively managed alternatives.

AJ Bell’s Manager versus Machine report revealed that fewer than a quarter of actively managed funds outperformed their passive counterparts over the past decade.

Ms Young said: “To cut costs, consider replacing persistent underperformers with tracker funds, or use a combination of the two approaches across different markets or regions.”

Her second recommendation involves setting up automatic monthly investments through platform services.

How would your ISA perform if you take AJ Bell’s advice?

|

AJ BELL

The ISA allowance resets each year on April 6, when a new tax year begins | GETTY

The ISA allowance resets each year on April 6, when a new tax year begins | GETTYThese typically offer discounted dealing charges compared with one-off trades, while also helping investors benefit from pound cost averaging by smoothing out market fluctuations.

The third strategy focuses on resisting the urge to tinker with holdings too frequently. Constant trading accumulates costs through bid-offer spreads, dealing fees and potentially stamp duty.

Ms Young shared: “Being disciplined with the number of times you check your investments and sticking to a plan on how often you review your portfolio will help.”

Her fourth tip concerns the choice between income and accumulation fund units. Those not requiring regular payouts should opt for accumulation units, which automatically reinvest dividends back into the fund rather than distributing them as cash.

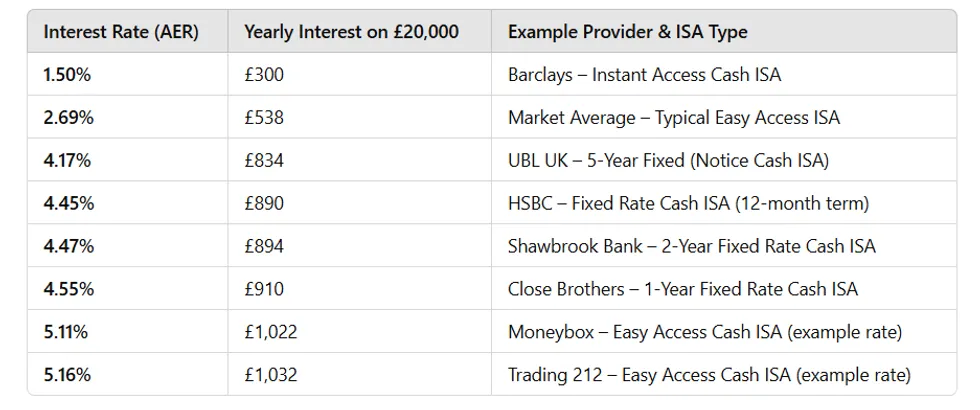

Examples of tax free Isa earnings in the UK if you had £20,000 in the Isa | GBN

Examples of tax free Isa earnings in the UK if you had £20,000 in the Isa | GBNThis approach eliminates the need to pay separate dealing charges when reinvesting income manually. It also reduces the administrative burden of managing multiple transactions throughout the year.

Ms Young’s final recommendation involves bringing multiple ISAs together with a single provider. While rule changes in 2024 permitted savers to contribute to several ISAs of the same type within one tax year, this flexibility can result in paying duplicate fees.

Purchasing identical shares across separate accounts means incurring dealing charges twice rather than once, however, analysts note that consolidation eliminates this inefficiency while simplifying portfolio management.

“Look for platforms that offer capped charges on shares and ETFs, and tiered charges for higher balances in funds,” Ms Young recommended.