Oil markets plunged deeper into turmoil on Sunday night as Brent crude surged beyond $104 per barrel (about £78), a level not seen since autumn 2023, raising fresh fears that the global economy could be heading toward another downturn.

Analysts at Goldman Sachs have warned the situation could worsen dramatically if conflict in the Middle East continues into April, with prices potentially climbing to $150 per barrel roughly £112.

Such a surge would push energy costs far beyond levels seen during previous crises and could feed directly into higher inflation, borrowing costs and slower economic growth.

For British households, the impact could be immediate.

Campaign group FairFuelUK warned that the pressure on drivers could worsen rapidly if crude continues climbing. Howard Cox from FairFuelUK said oil above $100 (around £74) per barrel could quickly translate into higher pump prices.

“If it goes over $100, we could see between 10p and 20p added to the price of fuel within weeks,” he said.

Mr Cox also warned that if oil reaches $120 per barrel roughly £90 the consequences could be severe for the wider economy.

“If it reaches $120, I believe it will trigger a recession,” he added.

Drivers now face the alarming prospect of petrol prices smashing through the previous record of 191.5p per litre, set during the energy shock that followed Russia’s invasion of Ukraine.

During that 2022 crisis, crude prices peaked at $116 per barrel (around £87). Current projections would exceed that level by a significant margin.

Some traders have issued even more severe warnings, suggesting oil could spike to $250 per barrel approximately £187 in extreme scenarios if supply disruptions intensify.

Such a jump would likely trigger a global economic shock, dramatically increasing fuel, transport and food costs while squeezing already stretched household budgets.

Oil prices surged past $100 per barrel for the first time since 2022

|

GETTY/tradingeconomic

Economists say a sustained oil shock would not only drive up petrol prices but also increase the cost of transporting goods, heating homes and producing food, raising the risk of inflation surging again just as many economies were beginning to stabilise.

Rachel Reeves will join finance ministers from the Group of Seven (G7) in an emergency call to discuss releasing global oil reserves after prices have surged.

The Chancellor will take part in the talks after crude oil jumped around 25 per cent overnight, sparking fears of a fresh global energy shock. Ministers are expected to discuss whether emergency oil reserves should be released in an effort to calm markets and stabilise prices.

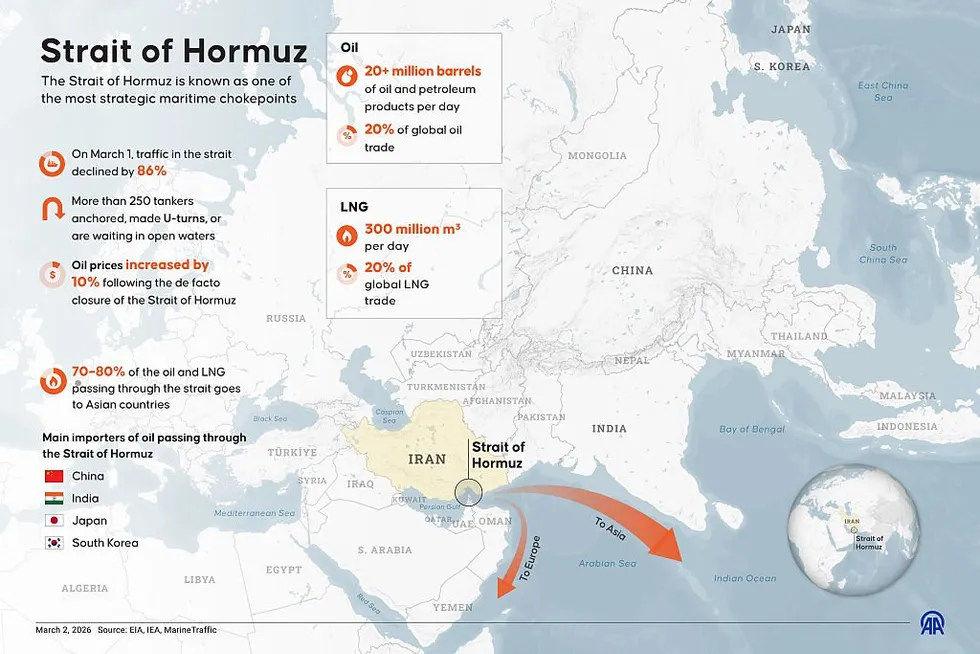

Prices surged as the US and Israel continued striking targets in Iran, raising fears of wider disruption to global oil supplies. Iran has threatened shipping through the Strait of Hormuz, one of the world’s most important oil routes.

Markets are already showing signs of strain as investors fear the energy crisis could derail fragile economic growth. In Japan, the benchmark Nikkei 225 fell 4.9 per cent to 52,909.30 as Asian markets were hit by the rising tensions.

The Strait of Hormuz is one of the most important shipping routes in the world, especially for oil exports | GETTY

The Strait of Hormuz is one of the most important shipping routes in the world, especially for oil exports | GETTYThe Strait of Hormuz lies at the heart of the crisis, with the vital waterway between Iran and Oman carrying roughly 20 per cent of global petroleum liquid consumption in 2024.

Goldman Sachs has warned that unless transit through this crucial shipping route returns to normal, oil could hit $150 by month’s end.

The strait has been effectively shut at times since US-Israel attacks on Iran began, with a senior adviser to Iran’s Revolutionary Guard threatening to “attack and set ablaze any ship attempting to cross”.

Qatar’s energy minister Saad al-Kaabi delivered a stark assessment of the potential fallout.

He said: “If this war continues for a few weeks, GDP growth around the world will be impacted. Everybody’s energy price is going to go higher. There will be shortages of some products and there will be a chain reaction of factories that cannot supply.”

The International Monetary Fund has sounded the alarm over the conflict’s wider economic consequences.

Trump says oil spike is a ‘small price to pay for peace’

|

TRUTH SOCIAL/DONALD TRUMPIMF managing director Kristalina Georgieva stated that a sustained 10 per cent increase in oil prices would drive global inflation up by 0.4 per cent.

“We are seeing resilience tested again by the new conflict in the Middle East,” Ms Georgieva said. “My advice to policymakers in this new global environment is think of the unthinkable and prepare for it.”

European LNG prices have surged more than 50 per cent since last week, with energy suppliers scrambling to respond.

Octopus founder Greg Jackson told Times Radio that markets were “in turmoil”, with his company raising fixed-price tariffs and introducing exit fees.

More than half of suppliers have reportedly reduced the number of fixed deals available to customers.

, a level not seen since autumn 202){kind=link}